Key Takeaways

- Financing used and refurbished medical equipment is mainstream — 84% of medical equipment acquisitions were financed by lease, loan, or line of credit in 2023

- Certified refurbished equipment is viewed more favorably by lenders than as-is used equipment

- Equipment age, condition documentation, and remaining useful life are the key eligibility variables

- Loans, leases, and SBA programs each serve different buyer profiles — knowing which fits your situation saves time and money

- Trade-in programs reduce or eliminate the need for external financing altogether

What Is Used and Refurbished Medical Equipment Financing?

Most healthcare facilities don't purchase endoscopic equipment outright. According to ELFA's 2024 Equipment Finance Industry Horizon Report, 84% of medical equipment acquisitions were financed by lease, loan, or line of credit in 2023 — making financing the standard approach, not the exception.

Used and refurbished medical equipment financing is a form of business financing that lets healthcare facilities acquire pre-owned or certified refurbished equipment without paying the full purchase price upfront. For high-cost devices like gastroscopes, colonoscopes, and bronchoscopes, this is often the only practical path to acquisition.

Financing pre-owned medical equipment does involve several considerations that standard small-business borrowers don't encounter:

- Equipment condition and certification status affect collateral value

- Lenders assess remaining useful life — not just purchase price

- Documentation requirements are stricter than for new equipment

- Lender risk tolerance varies based on the equipment's sourcing and maintenance history

Understanding these factors upfront helps medical buyers choose the right financing structure — and recognize when a trade-in program might eliminate the need for external financing altogether. This guide covers each consideration in detail.

Used vs. Refurbished Medical Equipment: Why the Distinction Matters for Financing

The terms "used" and "refurbished" are often treated as interchangeable. For financing purposes, they are not.

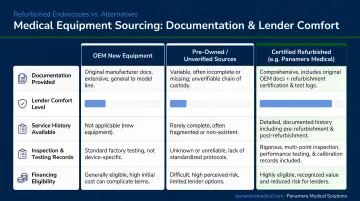

As-Is Used Equipment

As-is used equipment has changed ownership but received no formal restoration. It may come from auctions, private sellers, or facility liquidations. Condition is variable, documentation is often incomplete, and there's typically no warranty. Lenders treat this category with the most caution — the collateral value is harder to verify.

Certified Refurbished Equipment

Certified refurbished equipment has been restored to OEM or near-OEM performance standards. According to the FDA's 2024 guidance, proper servicing returns a device to its original safety and performance specifications. Equipment in this category typically comes with:

- Functional testing documentation

- Service and maintenance records

- Condition inspection reports

- A limited warranty (Olympus's Certified Pre-Owned program, for example, includes a one-year warranty)

Lenders view certified refurbished equipment as lower risk because the documentation supports a defensible collateral valuation — meaning better rates, longer repayment periods, and fewer requirements for additional collateral.

Three Sourcing Categories

| Source | Documentation | Lender Comfort |

|---|---|---|

| OEM-refurbished (e.g., Olympus CPO) | Comprehensive, manufacturer-backed | Highest |

| Third-party certified refurbished | Varies by dealer | Moderate to high |

| As-is used (auction, private sale) | Often minimal | Lowest |

For endoscopic equipment — gastroscopes, colonoscopes, bronchoscopes — lenders want evidence of remaining functional life and compliance with applicable servicing standards. Sourcing from a specialized dealer like Panamera Medical Solutions, with 15+ years in international endoscopy trading, typically makes the documentation process far more straightforward than buying through auction or private channels.

Lenders also tie maximum loan terms to remaining useful life. SBA 7(a) loans cannot exceed the equipment's useful life — so confirm manufacture date and expected functional lifespan before applying.

Benefits of Financing Used or Refurbished Medical Equipment

Cost Savings, Distributed

Certified refurbished endoscopes are substantially cheaper than new OEM equipment. MD Endoscopy, for example, states that certified pre-owned endoscopic equipment can save providers 50% or more compared with new — and lists refurbished video colonoscopes starting around $5,500–$7,000. Financing distributes this already-lower cost into manageable monthly payments, freeing capital for staffing, facility costs, or other operational priorities.

ELFA's 2024 equipment finance data shows why this approach resonates with healthcare buyers:

- 62% of equipment users cited cash-flow optimization as a top reason for financing

- 55% pointed to protection from obsolescence

Depreciation Already Absorbed

New equipment loses value fastest in its early years. Used and refurbished equipment has already absorbed that steep initial drop — meaning the asset holds its relative value more steadily over the loan term. You're far less likely to end up underwater on the loan before it's paid off.

Operational Availability

Refurbished equipment sourced through established dealers is typically available from existing inventory — no factory order queue, no extended lead times. For busy GI or endoscopy departments that need to expand capacity or replace a failed scope quickly, this matters.

Eligibility and What Lenders Look For

Credit Score and Business History

Requirements vary by lender type. Bank of America, for example, states it typically requires a personal credit score above 700 FICO, at least two years in business, and $100,000 in annual revenue. SBA programs don't publish a universal credit threshold, but they do have defined eligibility requirements.

Online and alternative lenders often set lower bars — credit scores below 700 can still qualify, particularly because the equipment itself serves as collateral, which reduces the lender's exposure compared to unsecured loans.

Equipment Age and Useful Life

Lenders tie loan terms to remaining useful life. SBA 504 loans, for instance, require long-term machinery and equipment to have at least 10 years of remaining useful life. SBA 7(a) terms cannot exceed the equipment's useful life regardless of what the borrower requests.

Confirm the manufacture date and expected functional lifespan before approaching lenders. Equipment near the end of its serviceable life will typically result in denials or very short, expensive terms.

Down Payment

Down payment requirements vary. U.S. Bank advertises equipment financing with no down payment required for qualifying borrowers. Bank of America notes that SBA financing may require as little as 10% down.

If the equipment's appraised value falls short of the loan amount, lenders may require additional collateral or a personal guarantee to close the gap.

Documentation Lenders Will Request

Pull these together before submitting any application:

- Equipment invoice or purchase quote

- Serial number and model details

- Condition/inspection report or professional appraisal

- Maintenance and service history

- Ownership transfer documentation from the seller

- Business tax returns (typically 2 years)

- Recent bank statements

- Profit and loss statement

Buyers sourcing through established certified refurbished dealers typically receive most of this documentation as part of the transaction. That's a practical advantage of working with a specialist over an auction or private seller.

Financing Options Available for Used Medical Equipment

Equipment Loans (Secured)

A dedicated equipment loan uses the purchased equipment as collateral. The borrower receives a lump sum, repays over a fixed term aligned with the equipment's useful life, and owns the equipment outright at the end. Interest rates are generally lower than unsecured alternatives because the lender has a recoverable asset. For high-value endoscopic devices, this is typically the most cost-effective financing path.

Equipment Leasing

Leasing allows the practice to use equipment for a monthly fee without immediate ownership. At term end, options typically include buying the equipment, renewing the lease, or returning it.

Leasing preserves more working capital upfront and may offer tax advantages — though consulting a tax adviser is essential before assuming any deduction eligibility. One key limitation: you don't build equity in the asset over time.

SBA Loans (7(a) and 504)

- SBA 7(a): Finances purchase and installation of machinery and equipment up to a $5M maximum. Rate caps are set by loan size — for loans above $350,000, the cap is the base rate plus 3.0%. Terms cannot exceed useful life.

- SBA 504: Designed for larger fixed-asset purchases. Requires at least 10 years of remaining useful life. Offers long-term, fixed-rate financing but involves stricter eligibility requirements and a longer application timeline.

Both programs offer competitive rates but require patience — processing times are longer than bank or alternative lender products.

Unsecured Business Term Loans and Lines of Credit

Practices with strong credit profiles may use an unsecured business term loan or line of credit. No collateral required, and funds can be used for any business purpose — not just equipment. The cost: higher interest rates than secured options. This structure suits practices that need fast access to capital or want to avoid tying specific assets to a loan agreement.

Step-by-Step Guide to Financing Used or Refurbished Medical Equipment

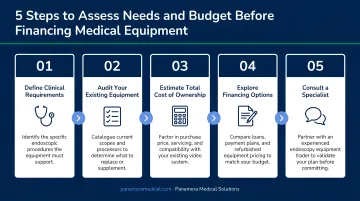

Step 1: Assess Needs and Budget

Before approaching any lender:

- Identify the specific equipment — model, manufacturer, specifications required

- Confirm equipment age and condition — get this from the seller before anything else

- Obtain a vendor quote — you'll need this for the loan application

- Estimate monthly payments — use an equipment loan calculator with your expected loan amount and term

- Determine available down payment — even a modest down payment improves approval odds

Step 2: Find the Equipment and Gather Documentation

Sourcing from a certified refurbished dealer rather than an auction or private seller simplifies this step. Reputable dealers provide invoices, serial number documentation, condition reports, and service history as part of the transaction.

Collect before applying:

- Vendor invoice or formal purchase quote

- Equipment serial number and model details

- Condition/inspection report

- Service and maintenance records

- Ownership transfer documentation

Incomplete documentation is among the most common reasons for financing delays or outright denials. Lenders need to assess equipment value and condition — a missing inspection report or serial number discrepancy can stall approval just as quickly as a credit issue.

Step 3: Compare Lenders and Apply

| Lender Type | Best For | Trade-Off |

|---|---|---|

| Traditional bank | Established practices, strong credit | Stricter requirements, slower approval |

| SBA lender | Larger purchases, competitive rates | Long processing times, more paperwork |

| Online/alternative lender | Newer practices, lower credit scores | Higher rates |

| Specialty medical equipment finance | Medical-specific knowledge, faster decisions | Fewer options, may require industry focus |

When evaluating offers, compare:

- Interest rate and APR

- Loan term length

- Origination fees

- Prepayment penalties

- Lender experience with used medical device financing specifically

Once approved, review the loan agreement before signing: focus on equipment ownership terms, default provisions, and any restrictions on use or location.

Trade-In and Buy-Back Programs: A Financing Alternative Worth Considering

Not every equipment upgrade requires a bank loan. Trade-in and buy-back programs — offered by endoscopic equipment dealers like Panamera Medical Solutions — let healthcare facilities exchange older scopes for credit toward replacement equipment, or receive direct cash payment for equipment they no longer need.

Panamera Medical Solutions accepts a wide range of equipment through these programs, including gastroscopes, colonoscopes, bronchoscopes, duodenoscopes, and video systems from Olympus, Pentax, Fujifilm, Karl Storz, and Stryker.

Why this matters for financing:

- Trade-in credit applied to a purchase reduces the loan amount needed

- A smaller loan improves loan-to-value ratios, which can unlock better terms

- For facilities upgrading one or two scopes at a time, trade-in value may cover enough of the purchase price to eliminate external financing entirely

- Documented trade-in credit may also serve as an effective down payment, which lenders often require for used equipment purchases

For facilities managing an aging endoscopy fleet, exploring trade-in value before starting the lender search is a logical first step.

Frequently Asked Questions

Can you get a loan on used equipment?

Yes — loans for used equipment are widely available. Lenders may impose stricter terms than they would for new equipment (higher rates, shorter terms, more documentation requirements), but strong condition documentation and sourcing from a reputable dealer makes approval more straightforward.

What credit score is needed for equipment financing?

Requirements vary by lender. Bank of America typically requires a personal credit score above 700 FICO for its small-business products. Online and alternative lenders often work with lower scores because the equipment serves as collateral, reducing the lender's risk compared to unsecured products.

How hard is it to get equipment financing?

Equipment financing is generally more accessible than unsecured business loans because the equipment itself serves as collateral. Used or refurbished medical equipment adds complexity, but buyers who prepare thorough documentation and work with experienced lenders tend to get through the process without major obstacles.

What is the difference between used and refurbished medical equipment for financing?

As-is used equipment has variable condition and limited documentation. Certified refurbished equipment has been restored to OEM or near-OEM standards, tested, documented, and often warrantied. Lenders view certified refurbished equipment more favorably — it's easier to establish collateral value, which typically results in better terms and higher approval rates.

How old can medical equipment be and still qualify for financing?

Lenders tie loan terms to remaining useful life, not a fixed age cutoff. SBA 504 loans require at least 10 years of remaining useful life; SBA 7(a) loans cannot exceed it. Confirm the manufacture date and functional lifespan with the seller before applying, as no lender will extend a 5-year loan on equipment with 3 years of life left.

What documents do I need to finance used medical equipment?

Expect to provide an equipment invoice, serial number and model details, a condition or inspection report, service history, business tax returns, recent bank statements, and seller ownership documentation. Certified refurbished equipment sourced from established dealers typically arrives with most of this already in order.